In spring 2026, Japan’s corporate governance framework is undergoing its most coordinated review in over a decade. Three parallel public consultations – the Ministry of Justice (MoJ) on Companies Act amendments, the Financial Services Agency (FSA) on revisions to the Corporate Governance Code, and the Tokyo Stock Exchange (TSE) on listing rules for minority shareholder protection – address a number of overlapping questions on capital flexibility, board oversight, shareholder rights, and disclosure. Should these proposals be enacted in their current form, their combined effect could materially reshape the balance between managerial agility and substantive minority shareholder safeguards. This ongoing wave of regulatory consultations continues with the Ministry of Economy, Trade and Industry (METI) launching a public consultation on the interpretation and guidance for the Guidelines for Corporate Takeovers. Collectively, these parallel reviews mark a pivotal moment in the evolution of Japan’s corporate governance regime, raising important questions about how the ensuing reforms will ultimately recalibrate the relationship between companies, boards, and shareholders(1).

Proposed reforms to corporate law, CG Code, and Listing Rules

The MoJ proposals relevant to corporate law focus on practical flexibility(2). If enacted, they would expand free share grants to employees of the company and its subsidiaries, broaden the share-delivery regime to permit staged increases in subsidiary stakes, ease in-kind contribution rules by replacing court-appointed inspectors with special-resolution shareholder approval plus board disclosure, lower the squeeze-out threshold from 90% to 66.7%, and introduce detailed rules for virtual-only meetings alongside a new beneficial owner identification system.

The FSA’s CG Code revisions aim to streamline the Code and shift emphasis from formal compliance to substantive governance and long-term value creation(3). Key changes include the removal or dilution of Principles 1.5 (anti-takeover measures), 1.6 (capital policies harmful to shareholders, including MBOs), and 1.7 (related-party transactions). Many Supplementary Principles are also downgraded to non-binding Interpretive Guidance. The revised Code strengthens focus on capital efficiency, cost-of-capital awareness, board effectiveness, skills matrices, diversity, and shareholder engagement. While intended to make the Code more concise and principles-based after more than a decade of implementation, some international investors have expressed concern that the changes could weaken structural accountability on minority shareholder protections.

The TSE’s listing rules changes seek to strengthen minority protections in quasi-controlled companies through revised director independence criteria, dissent-triggered disclosure and engagement obligations, and refined definitions of controlling shareholders(4).

Combined effects of the reforms on minority protections

Despite their different areas of applicability, the three sets of reforms intersect in a number of key areas, particularly on controlled-company transactions and minority safeguards. The MoJ’s proposed expansion of the share-delivery regime and reduction of the squeeze-out threshold would interact directly with the FSA’s proposed weakening of Code-mandated scrutiny on management buyouts (MBOs) and related-party transactions. This interplay creates a structural risk that ACGA has analysed in detail across its submissions.

MoJ proposal: Lower cash out thresholds but statutory majority-of-minority (MoM) protections

A notable positive in the MoJ proposal is the elevation of Majority-of-Minority (MoM) provisions to statutory level. Established as a recommended best practice under METI’s Fair Mergers and Acquisitions (M&A) Guidelines, the lower 66.7% squeeze-out threshold would now be available only if enhanced minority protections, including a mandatory MoM condition in the tender offer, are satisfied. This strengthens procedural safeguards in law and aims to make going-private transactions smoother whilst reducing coercive partial bids(5).

However, this improvement risks being outweighed by the broader reform package. A core concern is the interaction between the MoJ’s easier squeeze-out route and the FSA’s removal or dilution of Principles 1.5 (anti-takeover measures), 1.6 (capital policies harmful to shareholders, including MBOs), and 1.7 (related-party transactions) in the Corporate Governance Code. These principles previously imposed clear “comply-or-explain” expectations that boards must examine the necessity and rationale of such transactions, ensure appropriate procedures, and provide sufficient explanation to shareholders.

Although the FSA states these areas are already covered by disclosure obligations under the Companies Act, the Financial Instruments and Exchange Act (FIEA), and TSE listing rules, those provisions are primarily disclosure-focused and do not establish the same proactive expectations on board conduct and minority protections. By moving content into downgraded Interpretive Guidance under General Principle 1, these changes reduce structured accountability.

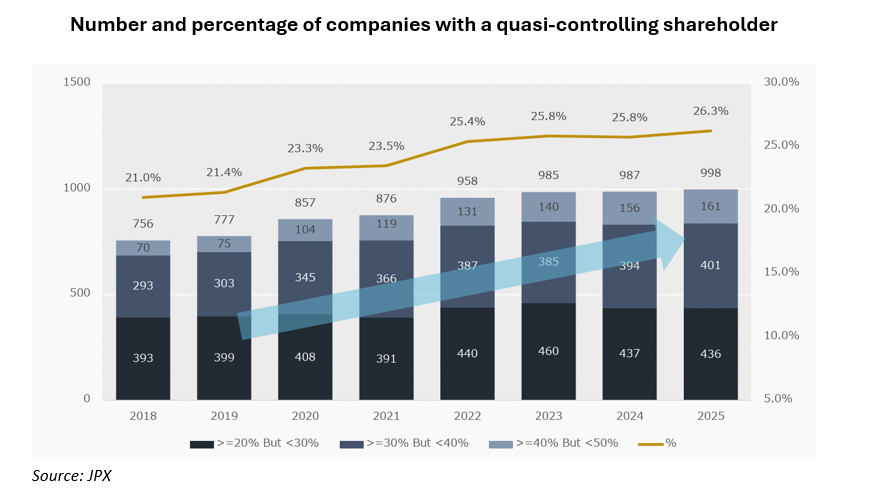

In Japan’s typical ownership structure, where a parent or quasi-controlling shareholder may hold up to 40–50%, supplemented by cross-shareholdings and management-aligned shares, a controlling bloc could realistically reach the new 66.7% threshold without broad minority support. The combination of an easier statutory route to cash-out and reduced soft-law expectations around procedural fairness therefore raises concerns about the overall level of minority shareholder protection. The TSE’s Study Group has reported on the growth in the number of companies meeting this criteria including an increase in the number of parent companies with capital ties at this level(6). To note, in the five years to 2025, the number of companies with a quasi-controlling shareholder increased from 857 to 998, or just over a quarter of companies listed on the market.

Application to other areas and real-world examples

The same logic applies to anti-takeover measures (Principle 1.5) and related-party transactions (Principle 1.7). Poison pills, which are seen more frequently in Japan than in most other major markets, could become easier to maintain without the comply-or-explain discipline of the Code. This would reduce pressure on boards to provide robust justification, making it easier for them to keep anti-takeover defences in place even if other legal requirements remain. ACGA’s February 2026 analysis of the Toyota Industries Corporation (TICO) privatisation identified gaps in special committee composition, majority-of-minority protections, and synergy disclosure even under the current Code; removing the principles would risk making such gaps structural rather than episodic.(7) Notable cases such as such as the TICO take-private proposal and ongoing activist campaigns at Nissan Shatai,(8) illustrate how intra-group transactions can disadvantage minority shareholders of listed subsidiaries.

The role of METI Guidelines vs the CG Code

The FSA’s proposal to remove Principles 1.5–1.7 is primarily based on overlaps with existing statutory requirements under the Companies Act, FIEA, and TSE listing rules. In practice, however, the more detailed operational guidance for boards in conflicted transactions comes from METI’s 2019 Fair M&A Guidelines (for MBOs and controlling shareholder deals) and the 2023 Guidelines for Corporate Takeovers. These have become a key practical reference for boards, setting out specific best practices including independent Special Committees, fairness opinions, market checks, and board neutrality.

Recent cases illustrate this shift. In the TICO take-private (2025) and the Makino Milling Machine takeover battle (2024–2025),[9] boards, activists, courts, and investors relied predominantly on the METI Guidelines and TSE rules rather than the CG Code. Nevertheless, downgrading Principles 1.5–1.7 indicates a regressive step. While high profile deals attract strong external scrutiny, METI guidelines remain voluntary and lack the market-wide “comply-or-explain” discipline and visibility provided by the CG Code. This may reduce accountability in lower-profile or less scrutinised transactions.

Further areas of overlap between the consultations

Improving Yuho disclosure timing ahead of AGMs

A further area of constructive overlap concerns the timing and integration of corporate disclosures ahead of the annual general meeting (AGM). Japan’s complex reporting requirements have long been a concern for international investors, particularly the late delivery of the Yuho (Annual Securities Report). Many companies still release these reports on the day of, or even after, the AGM, limiting shareholders’ ability to make informed voting decisions(10).

The FSA’s CG Code consultation proposes requiring listed companies to provide their Yuho at least three weeks prior to the AGM(11). The MoJ’s Companies Act consultation complements this by proposing greater flexibility in reporting obligations. Companies would no longer be required to produce both a separate Business Report and Yuho if they can integrate the required information into a single document within a “certain period” before the AGM(12).

This coordination between the FSA and MoJ is a welcome development aimed at reducing duplication while improving timeliness. However, its effectiveness will depend on careful alignment. For the reforms to deliver genuine benefits to shareholders, the “certain period” in the MoJ proposal should be set at a minimum of three weeks (21 days) before the AGM — consistent with the FSA’s proposal and international best practice in other developed markets.

To ensure this outcome, investors have advocated that the FSA should elevate the three-week Yuho disclosure requirement from Interpretive Guidance to a formal Principle in the CG Code. A shorter period would undermine the goal of enabling informed shareholder participation and weaken the overall impact of both initiatives. A watered-down compromise, such as leaving the three-week requirement in non-binding guidance, could ultimately satisfy neither corporate efficiency goals nor investor expectations for meaningful transparency and engagement.

Strengthening the minority voice: Voting dissent obligations

Another area of constructive overlap is the proposed voting dissent mechanism aimed at strengthening the minority shareholder voice, particularly in companies with controlling or quasi-controlling shareholders.

The FSA’s CG Code consultation encourages boards to analyse the reasons for significant opposing votes and take appropriate follow-up actions(13). The TSE’s consultation on revisions to the Listing Rules Regarding Minority Shareholder Protection introduces specific disclosure and engagement obligations, applicable to companies with a controlling or quasi- controlling shareholder (defined in the proposal as those where a shareholder or group holds 40% or more of the voting rights). It requires enhanced explanations and engagement plans when a significant portion of minority votes (currently proposed at over 50%) opposes a resolution, particularly in director elections.

This coordinated effort is welcome progress. However, the effectiveness of the mechanism will depend heavily on the thresholds used to trigger these obligations. The current proposed thresholds appear somewhat arbitrary and too high to be meaningful in practice. ACGA and international investors have advocated for a more reasonable trigger level, such as 20% of minority votes cast against a resolution. A threshold that is too high risks rendering the mechanism largely ineffective, while one that is too low could create unnecessary burden.

For this reform to deliver real accountability in controlled companies, the final threshold in both the TSE Listing Rules and the CG Code should be calibrated at a level that provides genuine protection for minority shareholders.

Strengthening director independence

Director independence is a key area addressed in both the FSA and TSE consultations. The FSA’s CG Code revisions elevate the expectation that companies with controlling shareholders should have a sufficient number of independent directors to a formal Principle (requiring majority independence for relevant Prime Market companies), while also placing greater emphasis on board effectiveness, skills diversity, and strategic alignment. The TSE’s Listing Rules consultation tightens the definition of independence by expanding disqualification criteria, particularly for individuals with material ties to major or controlling shareholders. Whilst we welcome these steps, the revisions still fall short on ensuring the practical effectiveness of independent directors, including clearer expectations for the role of a Lead Independent Director and more rigorous board evaluation processes.

Collectively, these reforms reflect a more developed attempt to tackle the longstanding weakness of board independence in Japan’s corporate landscape. However, their ultimate success will hinge less on formal rules and more on whether they can drive a genuine cultural shift in boardrooms. Simply tightening definitions or elevating expectations to Principles will have limited impact if independent directors continue to function primarily as formalistic checks rather than as active challengers of management and controlling shareholders. True independence ultimately requires a deeper change in mindset and boardroom dynamics.

Balancing Reform Ambition with Shareholder Protections

Japan’s market context makes these proposals particularly salient. Despite genuine progress since 2015 – independent directors now exceed one-third on Prime Market boards and cross-shareholdings have declined – structural features remain: roughly 26% of listed companies still have quasi-controlling shareholders, many listed subsidiaries deliver sub-8% ROE, and relational capital allocation persists. High-profile episodes such as Toyota Industries, TBS Holdings’ poison pill renewal without shareholder approval,(14) and Nidec’s oversight shortcomings demonstrate that formal compliance does not always translate into substantive protection.(15)

For long-term investors, the net impact of the three reforms, if implemented as currently proposed, will depend on final calibration and coordinated implementation. Key watchpoints include whether the FSA retains meaningful Code principles and subjects important guidance to comply-or-explain discipline, whether the MoJ limits the scope of its flexibility proposals (especially on share deliveries and squeeze-outs), and whether the TSE’s thresholds and independence criteria deliver real accountability. Without careful alignment, the package could inadvertently create a more controller- and management-friendly environment, reducing minority leverage and potentially affecting valuations and foreign capital flows.

On the economic side, the MoJ’s intent is clear: easier cash-outs and staged share deliveries are designed to promote more efficient M&A, reduce prolonged uncertainty in partial bids, and allow better operational integration of subsidiaries – outcomes that could improve capital allocation, ROE, and overall corporate competitiveness. Yet if minority protections are materially diluted, the reforms risk undermining investor confidence, discouraging minority capital, and ultimately harming the depth and liquidity of Japan’s equity markets.

Meanwhile, METI has just launched a consultation on Japan’s M&A Guidelines.(16) These are meant to provide Interpretation of the provisions of the 2023 guidelines, which have been credited with significantly increasing takeover proposals: deal value in 2025 surged by 175% compared to the previous year.(17) The current consultation on the interpretation of these M&A guidelines, however, are to provide a framework for non-price considerations which boards may determine supersede over price in determining which bids are favoured. Not surprisingly, there is significant concern that this could be used defensively by management to ward off takeover proposals and would test the real effectiveness of board oversight to protect the interests of shareholders.

Japan’s policymakers have an opportunity to demonstrate that modernisation and minority protection are complementary, not contradictory. ACGA’s coordinated commentary across the consultations underscores the importance of this balance. The ultimate success of the 2026 reforms will be measured not by legislative volume but by whether they sustain the reform momentum towards shareholder value and in turn investor confidence in Japan’s long-term corporate governance journey.

Footnotes

1. https://www.meti.go.jp/english/press/2026/pdf/0618_001a.pdf

2. https://public-comment.e-gov.go.jp/pcm/detail?CLASSNAME=PCMMSTDETAIL&Mode=0&id=300080352

3. https://www.fsa.go.jp/en/news/2026/20260410.html

4. https://www.jpx.co.jp/rules-participants/public-comment/detail/d1/20260327-01.html

5. https://www.meti.go.jp/policy/economy/keiei_innovation/keizaihousei/pdf/fairmaguidelines_english.pdf

6. https://www.jpx.co.jp/english/equities/follow-up/b5b4pj000004yqcc-att/vk0khi000000ld1e.pdf

7. https://www.acga-asia.org/blog-detail.php?id=114

8. www.asahi.com/ajw/articles/15862785https://www.asahi.com/ajw/articles/15862785

9. https://asia.nikkei.com/business/business-deals/japan-s-nidec-seeks-takeover-of-machine-tool-maker-makino

10. https://www.acga-asia.org/pdf/acga-open-letter-prioritization-of-annual-reports-before-agms

11. This recommendation is currently placed in the Interpretive Guidance under Principle 1-2 (Securing Shareholder Rights).

12. Section III-2 of the MoJ interim draft on disclosure and shareholder meeting materials.

13. Revised Principle 1.3 (Company Proposals that are Opposed by a Considerable Number of Shareholders at General Shareholder Meetings).

14. https://corporate.vanguard.com/content/dam/corp/advocate/investment-stewardship/pdf/policies-and-reports/2025_japan_regional_brief.pdf

15. https://www.acga-asia.org/blog-detail.php?id=112

16. Invitation for Public Comments on Drafts of the Interpretation, Key Points and the Q&A on the “Guidelines for Corporate Takeovers”

17. Japan: A Corporate/M&A: Domestic Overview Law | Chambers and Partners

About the Author(s)

Dr Helena Fung

Dr Helena Fung

Head of Research and Advocacy, ACGA

As Head of Research and Advocacy, Helena leads the research team and coordinates advocacy efforts across the Asia region, working closely with the ACGA’s Secretary General and secretariat team. Dr. Helena Fung (馮伊蓮娜) joined the ACGA in April 2025, prior to which she worked for the London Stock Exchange Group as Head of Sustainable Finance and Investment, Asia Pacific, where she was responsible for strategy, expansion and product development across the region, focused on indexes, data and analytics solutions. A core part of her role was regulatory engagement with policy makers and standard setters and stock exchange partnerships focusing on sustainability initiatives. Helena relocated to Hong Kong in 2014 from London - a key hub for ESG investments, where she worked for the responsible investment arm of Hermes Investment Management, enabling pension funds and asset managers to integrate sustainability criteria into passive and active portfolios. Helena’s experience includes ESG integration, equity analysis and advising on philanthropy for family office, asset management and institutional clients. She has been working in ESG and Sustainable Investment since 2008, including providing advisory research on stewardship implementation for pension funds and family office clients, drafting responsible investment policies and integrating sustainability policies into both active and passive portfolios. Helena has postgraduate qualifications in law and holds a professional investment qualification and a Ph.D. from the University of Glasgow.