The price of enterprise: balancing governance and incentives

by Anuja Agarwal, Hetal Dalal

Enterprise as a factor of production encompassing vision, risk-taking, and managerial acumen has long been recognised as a critical catalyst that transforms other factors of production into corporate value. Appropriate compensation is essential to attract leadership able to drive enterprise. This commentary therefore examines recent trends in executive pay in India following the 2025 proxy voting season, drawing on analysis from IiAS and ACGA to assess whether governance mechanisms are keeping pace with rising packages.

India’s executive pay regime has evolved sharply over five decades. In November 1969, the Department of Company Affairs capped director pay at ₹7,500 per month(1)under the Companies Act 1956, later reducing it to ₹5,000 with central government approval needed for any excess.(2) The economic liberalisation of 1991 progressively dismantled these controls, and since September 2018, prior government approval is no longer required for paying directors above the statutory limit. Today, even this statutory ceiling of 11% of net profits can be exceeded through a special shareholder resolution.(3)

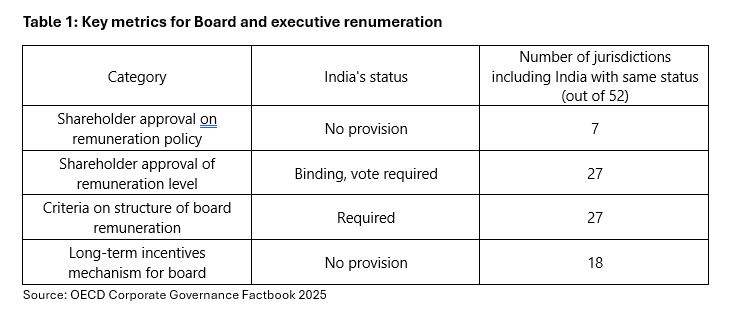

The following table from the OECD Corporate Governance Factbook 2025 shows India’s position among 52 jurisdictions on board and key executive remuneration areas.(4) For example, India has no requirement for shareholder approval of remuneration policy (a position it shares with just six other jurisdictions while 45 jurisdictions do require it); although a nomination and remuneration committee (NRC) must develop the policy, it is not subject to shareholder vote. Shareholder approval is, however, required for the level of renumeration, a status shared by 27 out of 52 jurisdictions.

Recent compensation trends

The consequences of decontrol are visible in the data. Among BSE 200 constituents, the median total remuneration for CEOs stands at approximately ₹8.2 crore (approximately US$990,000)(5) in FY2024-25, with significant dispersion: 39% of CEOs earn below ₹5 crore, while the top decile – dominated by technology and financial services companies – exceeds ₹50 crore. At the 75th percentile, packages reach ₹22.3 crore, driven by banking, financial services and insurance firms, IT services, and large-cap consumer goods companies.

The three highest-paid CEOs in the BSE 200 are all professional, non-promoter executives: Sudhir Singh of Coforge (₹197.7 crore), Yashish Dahiya of PB Fintech (₹146.7 crore), and Sandeep Kalra of Persistent Systems (₹125 crore). Among promoter-CEOs, Pawan Munjal of Hero MotoCorp (₹109.4 crore) and Murali K. Divi of Divis Laboratories (₹88.2 crore) are the highest earners. Compensation structures have shifted toward performance-linked pay: across BSE 200 executive directors, fixed compensation represents approximately 44% of total remuneration in aggregate, with the remaining 56% tied to variable outcomes including EBITDA, cash flow, and at times, ESG metrics.

A structural divergence is evident between promoter and executive management CEOs. The median total remuneration for promoter-CEOs in the BSE 200 is ₹18.8 crore (US$2.03 million) - more than three times the ₹5.7 crore (US$612,500) median for non-promoter professional CEOs. This gap reflects the reality that promoter-CEO packages are, in structural terms, self-approved.

Is widening pay disparity leading to brain-drain?

Pay disparity in India compounds governance concerns. CEO-to-median-employee pay ratios at BSE 200 companies with available data show a median of 92:1, but at the upper end the numbers are extreme: Divis Laboratories tops the dataset at 1,589:1 (Murali K. Divi), followed by Shree Cement at 900:1 (H. M. Bangur), Persistent Systems at 882:1 (Sandeep Kalra), and Tech Mahindra at 840:1 (Mohit Joshi). Infosys reports a CEO pay ratio of 290:1 for Salil Parekh in FY2024-25. The mean pay ratio across the BSE 200 dataset is 169:1, almost double the median of CEO salary to average employee illustrating a relatively small group of companies that significantly skews the ratio. While the US is an outlier with an average CEO to median employee pay ration of 285:1 for S&P500 companies in 2024,(6) a 2018 study showed that India was not far behind, with its average ratio surpassing those of the UK, Netherlands, Switzerland, Canada and China.(7)

Such extreme pay disparity raises concerns about a potential brain drain. India’s outward migration of skilled talent is well documented, and the acceleration of this trend in recent years has coincided with the period of fastest executive pay growth. Technology and financial services – the sectors driving the highest CEO packages – contribute disproportionately to outflows of mid-level and senior professionals. This reflects a structural challenge: the companies facing the greatest difficulty retaining their talent pool are paying more to retain their CEOs relative to the layers below them.

Equity-based compensation has become central to executive retention. Employee stock ownership plan (ESOP) income for executive directors across the BSE 200 totalled ₹1,443 crore (approximately US$155 million) in FY2024-25, spread across just 93 individuals. However, transparency concerns persist. IiAS research reveals that 61% of ESOP resolutions had over 20% institutional investor dissent with 12% rejected outright. Under Indian regulations, promoters are prohibited from receiving ESOPs. In many new-age companies, founders have sidestepped this restriction by not classifying themselves as promoters, allowing them to receive ESOPs.

Governance conflicts

Yet the more troubling dimension of Indian executive compensation lies not in quantum but in governance architecture. Promoters (controlling shareholders) who frequently serve as executive directors are permitted to vote on their own remuneration resolutions as these are not classified as related party transactions under the Companies Act or SEBI (Listing Obligations and Disclosure Requirements) 2015 (SEBI LODR). This creates a structural conflict of interest: promoters effectively act as judge in their own cause. Between January 2023 and September 2024, only ten of 893 promoter remuneration proposals were rejected while institutional dissent was ignored in 216 cases. IiAS’ analysis reveals that 24.5% of promoter pay resolutions during that period would have failed if subject to a majority-of-minority vote.

The argument that regulations prevent promoters from participating in remuneration decisions is only partially accurate. The law explicitly prohibits ‘interested directors’ from voting on board resolutions in which they have a personal interest – yet it does not explicitly prohibit them from being present or participating in the specific discussion. Promoters are even allowed to become members of the Nomination and Remuneration Committees because Indian regulations do not mandate a completely independent committee composition. Therefore, in practice, promoters can influence their pay decisions, independent of the regulatory guardrails.

Additionally, when pay exceeds regulatory thresholds (5% of profits for one director, 10% for all promoters) a shareholder resolution is required. Because promoters typically hold a high percentage of shares, they generally vote in favour of these resolutions despite overwhelming opposition from public shareholders.

In addition, gender pay disparity persists stubbornly at the apex. Among BSE 200 CEOs with disclosed remuneration data, women account for just 17 of 262 individuals, representing only 6.5% of the CEO population for constituents of India’s large and mid-cap index. The median total remuneration for female CEOs is ₹6.9 crore, versus ₹8.5 crore for male CEOs, representing a median pay gap of 19.6%. On a mean basis the gap is more severe: female CEO mean remuneration is ₹8.4 crore against ₹17.4 crore for male CEOs – a gap of 51.7% – driven by the concentration of male CEOs in technology companies with high long-term incentive structures. Female CEOs are most prominently represented across four sectors: pharmaceuticals (Vinita Gupta at Lupin, Madhurima Singh at Alkem), financial services (Vibha Padalkar at HDFC Life, Vishakha Mulye at Aditya Birla Capital), consumer/retail (Falguni Nayar at Nykaa), and healthcare (Suneeta Reddy and Sangita Reddy at Apollo Hospitals).

These findings from the BSE 200 dataset align closely with the CFA Institute and CFA Society of India’s Mind the Gender Gap, Edition 3 report published in February 2026, which examines mandatory Business Responsibility and Sustainability Reporting (BRSR) disclosure data for 300 listed companies across FY2022–23 to FY2024–25.(8) The report finds that female board directors earned just 27.4% of the remuneration of their male counterparts in FY2024–25, a deterioration from 38.2% the prior year as male director remuneration accelerated. At the Key Managerial Personnel (KMP) level, the picture is somewhat better: female KMP earned 59.3% of male KMP remuneration in FY2024–25, improving from 48.6% in FY2022–23.

Yet almost two-thirds of sample companies have no female KMP at all, and for every seven male KMPs there is less than one female KMP. The upstream pipeline problem is real: despite women constituting 43% of STEMM (science, technology, engineering mathematics and medicine) enrolments in higher education, their representation at the CEO and KMP tiers of listed companies remains minimal.(9)

Remuneration voting trends 2025: Companies with defeated resolutions

The 2025 proxy voting season has crystallised these tensions. IiAS analysed 1,252 remuneration resolutions for the year to October 2025, with 33% attracting over 20% institutional dissent and 16 resolutions rejected outright: higher than the 1-in-200 historical defeat rate.

Companies with defeated remuneration resolutions included:

• Gokaldas Exports Limited: ESOP resolution that allowed stock options at a 20% discount to market price, with nearly 43% of the total pool directed to the CEO.

• Lumax Auto Technologies Limited: Dual executive positions held by promoters, with board pay significantly skewed towards them.

• Paras Defence and Space Technologies Limited: Uncapped pay and unclear basis for variable pay.

• Bliss GVS Pharma Limited: Large sweat equity grants resulting in high compensation, estimated at nearly 12% of pre-tax profits.

• Crompton Greaves Consumer Electricals Limited: ESOP grants issued at face value, with poor disclosure on vesting terms and performance conditions.

• IPCA Laboratories Limited: ESOP grants at a 65% discount to market price.

• APL Apollo Tubes Limited: Excessive NRC discretion on ESOP exercise price and vesting conditions.

In contrast, at other companies, several notable best practices stood out.

• Infosys provided detailed disclosure on CEO Salil Parekh’s compensation of ₹80.62 crore(10) (approximately US$9.3 million) in FY2024-25 at a stated pay ratio of 290:1, and gives disclosures on performance-based stock options, future ESOP grants, performance metrics (including ESG linkage), and five-year pay estimates with peer benchmarking.

• Schaeffler India capped short-term bonuses (Free Cash Flow 40% weight, Schaeffler Value Added 40%, non-financial targets 20%). Long-term incentives were linked to three key metrics: service/ tenure (50% weight); Total Shareholder Returns (TSR 25%); and climate neutrality targets (25%), with absolute remuneration ceilings.

• Kotak Mahindra Bank granted stock options at market price with 100% performance-based vesting tied to book value per share, ROE, asset quality, and profitability metrics.

• HDFC AMC disclosed performance parameters with indicative weights, capping minimum weight per parameter at 25%.

Structural challenges and reform opportunities

Several key structural reforms are required to strengthen remuneration practices in India and to address practices such as bundling of appointment and remuneration resolutions which obscures independent evaluation, and the lack of transparency in target-setting around KPIs, performance thresholds, and achievement levels.

Perhaps the most important structural reform required is to prevent promoters from voting on their own compensation packages. Removing this clear conflict of interest would help moderate excessive pay levels and significantly improve accountability through better disclosure and oversight.

In India, shareholder approvals for managerial remuneration – governed by Section 197 of the Companies Act 2013 and SEBI LODR Reg. 17(6) – are typically granted for periods of up to five years through an ordinary or special resolution. This becomes particularly important when the proposed remuneration exceeds 11% of the company’s net profits, as crossing this statutory ceiling requires shareholder approval via a special resolution.(11)

The board, through its Nomination and Remuneration Committee, must conduct annual reviews of remuneration and make adjustments for performance. However, full shareholder re-approval is not required annually as it is linked to the tenure of the original approval (often five years).(12) This structure creates a key misalignment: limited shareholder scrutiny despite the board’s annual adjustments to pay.

Remuneration committees should comprise only independent directors with no promoter family members. Given that women constitute only 27.3% of BSE 200 independent directors, actively improving gender diversity on nomination and remuneration committees is essential to addressing the executive gender pay gap. Both ACGA and IiAS advocate for clearer ESOP disclosure in the annual report, specifically detailing performance targets and achievements that led to the vesting of options. Where shareholder dissent is significant, for instance exceeding 20%, companies should be required to provide a mandatory explanations in response.

Independent non-executive directors (INEDs) face a separate challenge. The median sitting fee paid to independent directors across the BSE 200 is ₹10.5 lakh per year (about US$11,320), with median total remuneration including commission is ₹39.5 lakh (US$42,655). The statutory cap of ₹1 lakh (about US$1,000) per meeting on sitting fees is incongruous when these same directors are asked to scrutinise and approve executive packages reaching into the tens of crores. The highest total remuneration received by a BSE 200 independent director in FY2024-25 was ₹316 lakh (US$341,250) paid by Infosys to Michael Gibbs. For female directors, the gender pay gap persists. Whilst SEBI’s mandate for at least one female independent director has raised the floor, it has not driven substantive integration. There needs to be increased female representation on key committees like remuneration and nomination in order to address the gender pay gap.

Stewardship conversations underscore the urgency to address misalignment in the approach to compensation structures. Investor participants in ACGA's 2025 India delegation, as well as IiAS have recommended excluding promoter votes on self-compensation, unbundling resolutions, and mandating variable pay metric disclosure.(13) IiAS has further advocated for a mandatory Shareholder Dissent Review Mechanism for votes receiving over 20% minority shareholder dissent, with both board engagement and four-month disclosures, an approach that ACGA supports.(14)

The following amendments would further strengthen oversight without curbing pay flexibility:

• Exclude promoter votes on self-remuneration items and adopt majority-of-minority voting, recommended by IiAS as well as ACGA in an open letter in 2025.(15)

• Unbundle appointment and pay resolutions to allow for separate voting on these two components of appointments and re-appointments of directors.

• Shift to annual approvals for variable pay, with full disclosure of KPIs and thresholds. Several banks already do this, but most of corporate India does not.

• Mandate ESOP details on grants, allocations, performance criteria for vesting and subsequent annual review of targets achieved for vesting to be recommended or approved by the board.

• Introduce a Shareholder Dissent Review Mechanism where there is significant minority shareholder dissent (e.g. 20% proposed by IiAS), requiring board engagement and disclosures - similar to UK/EU “comply or explain” post-dissent practices.

Investors appreciate that enterprise is the magic ingredient in corporate value creation. Boards may approve higher than average compensation, provided it is transparent, performance-linked, and subject to genuine shareholder oversight. The true challenge from a governance standpoint lies in balancing these incentives without succumbing to entrenched conflicts.

Footnotes

1. ₹7,500 in 1969 equals 1,000 USD at the historical exchange rate of 7.5 INR per USD. The equivalent purchasing power today would be about ₹91,713 INR or using 91.71 as exchange rate still around 1000 USD

2. https://corporate.cyrilamarchandblogs.com/2024/07/managerial-remuneration-should-promoters-be-disenfranchised/

3. Section 197(1), read with Schedule V, Companies Act, 2013, permits total managerial remuneration in a public company to exceed 11% of net profits (computed under Section 198) if authorised by shareholders in general meeting, subject to the conditions in Schedule V

4. https://www.oecd.org/en/publications/oecd-corporate-governance-factbook-2025_f4f43735-en.html

5. 1 million USD equals approximately 8.4 crore INR at current exchange rates. 1 crore = 10 million INR

6. Executive Paywatch - 2025 | AFL-CIO

7. Pay gap between CEOs and workers by country 2018| Statista

8. https://rpc.cfainstitute.org/research/reports/2026/mind-gender-gap-edition-3

9. Compareye BSE200 data set

10. https://www.infosys.com/investors/reports-filings/annual-report/annual/documents/infosys-ar-25.pdf

11. Exceeding regulatory thresholds require special majority. Also, there is a 5% of profits cap for the MD, and 10% for all EDs put together.

12. Banks often seek annual shareholder approval, particularly for variable pay, aligning with RBI guidelines (e.g., Compensation Framework 2020 caps variable at 200–300% of fixed, with annual oversight).

13. https://www.acga-asia.org/advocacy-detail.php?id=520&sk=&sa=

14. https://www.iiasadvisory.com/institutional-eye/2024-shareholder-meetings-review-data

15. https://www.acga-asia.org/advocacy-detail.php?id=520&sk=&sa=

Download File Disclaimer

In addition to the ACGA website disclaimer access to the "Members' Area" of the ACGA website is subject to the general disclaimer and content attribution statements below.

General Disclaimer

By logging into our Members' Area you acknowledge that all materials displayed on the site or made available for download are for the exclusive use of ACGA members. You may not share the content with parties outside of your organisation.

Content Attribution

The copyright ownership of all material on our website belongs to ACGA. Should you wish to use any materials in the course of your corporate research, including directly quoting or paraphrasing sections, reprinting, reproducing or the like, we request that you give proper acknowledgement to ACGA and share a copy with us. Please email mikky@acga-asia.org.