Following Korea’s third wave of Commercial Code amendments - what comes next?

by Yura Ahn, new Research Head for Korea

This is Yura’s first commentary since joining ACGA as Research Head for Korea.

Korea's legislature has addressed one of the most persistent tools of entrenched control: treasury shares. This has been marked by a significant wave of treasury share cancellations by major listed companies. In this article, we evaluate the impact of the recent “third wave” of Commercial Code amendments and examine how legislative attention is now turning to the Business Judgement Rule.

Korea's corporate governance reform has unfolded in distinct waves. The first two amendments extending directors' duty of loyalty to shareholders and mandating cumulative voting alongside expanded separate elections for audit committee members were covered in earlier ACGA commentaries (click here and here). Both were significant. However, seasoned observers of the Korean market have long argued that without addressing the structural misuse of treasury shares, even the most robust board reforms would leave a critical loophole intact. The third wave of Commercial Code amendments, passed by the National Assembly in February, takes direct aim at closing that loophole. Looking ahead, we view the drafting of the Business Judgement Rule as significant in shaping the liability structure of these reforms.

The third Commercial Code amendment

The latest amendments target the use of repurchased shares not for shareholder returns, but as a mechanism to entrench controlling shareholders and suppress minority influence. In Korea, treasury shares have historically been used often as a lever of corporate control. Treasury shares were deployed in friendly share swaps between affiliated companies, allocated to holding structures during spin-offs or retained as a buffer against unwanted shareholder pressure. In the absence of a mandatory cancellation requirement, repurchased shares could be held indefinitely, creating a permanent reservoir of latent voting power available to insiders and potentially weakening the impact of earlier reforms.

Three provisions stand out:

1. First, companies will in principle be required to cancel treasury shares within one year of acquisition. Existing holdings benefit from a grace period: in practice, companies have up to 18 months from the law's effective date to comply with pre existing positions. Exemptions cover retention for employee stock ownership plans, compensation schemes, and certain other managerial purposes, subject to shareholder approval.

2. Second, the law curtails the so-called "spin-off magic." When a company spun off a subsidiary under the previous regime, newly issued shares of that subsidiary were allocated to the parent company's treasury share account, allowing controlling shareholders to increase their effective voting power in the newly listed entity without diluting their own stake in the parent.

3. Third, stricter disclosure requirements apply to any disposal of treasury shares to third parties, designed to uphold the principle of shareholder equality.

Taken together, the reforms address a structural imbalance that has long undermined investor confidence. Under the previous regime, treasury shares were nominally "off the table" for voting purposes but remained potent tools for controlling shareholders through strategic deployment in mergers, spin-offs, and friendly cross-shareholding arrangements. The new rules do not eliminate all flexibility. Shares reserved for employee compensation schemes are carved out. Even so, the reforms significantly narrow the discretionary space that has historically been exploited.

Corporate resistance and realignment

The legislative debate has not been without friction. Business lobby groups, including the Korea Chamber of Commerce and Industry and the Federation of Korean Industries, have framed mandatory cancellation as a vulnerability(1): they argue the regulation will expose Korean companies to "hostile" foreign activist funds(2). This line of reasoning is familiar. It has also been deployed against most significant governance reforms in Korea over the past decade.

A related legislative development worth monitoring is the push to codify the Business Judgment Rule (BJR). Unlike in the United States or many European jurisdictions, Korea currently has no statutory BJR so directors seeking protection from liability must rely on general civil law principles and evolving case law. Proponents argue it would provide directors with a necessary safe harbour in the wake of expanded liability. The drafting will matter: a well-calibrated BJR is a legitimate governance instrument in many markets, but its scope in the Korean context will warrant close attention.

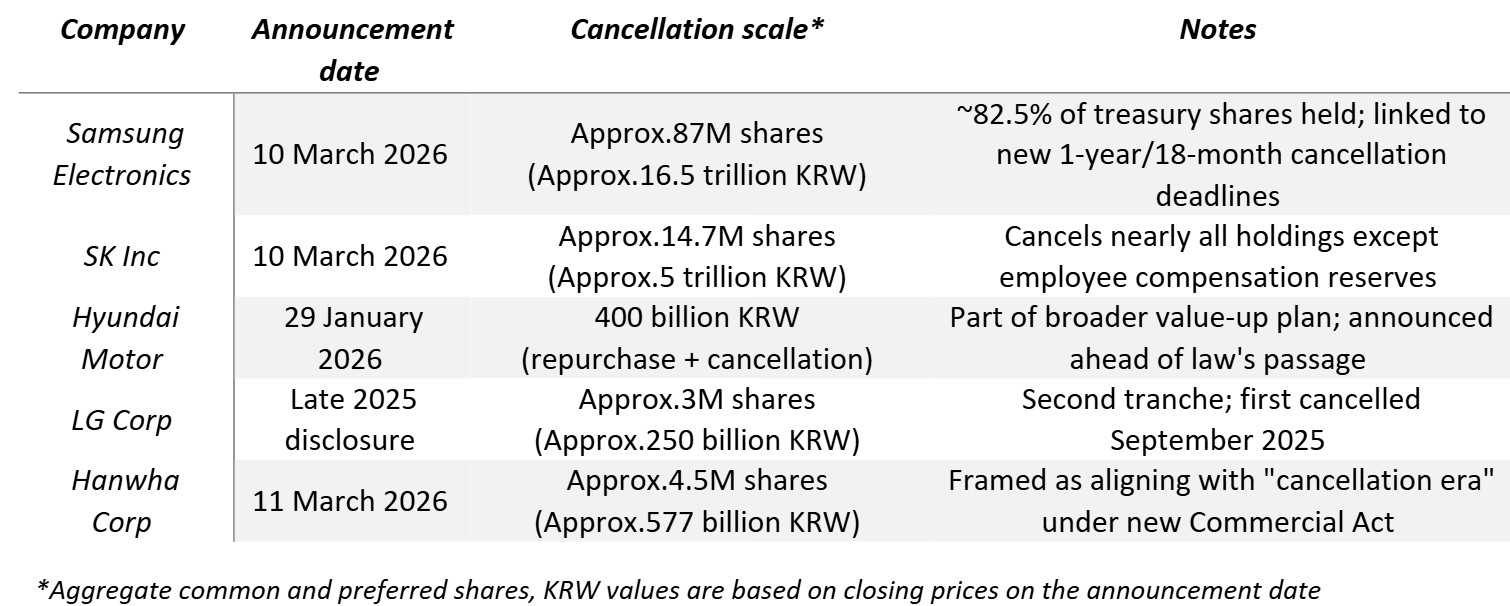

On the ground, a more pragmatic corporate response has also emerged. Even before the law's full implementation, a number of key companies such as the holding company or crown jewels of the conglomerates have moved proactively, announcing large-scale cancellations framed as shareholder-value initiatives, and in some cases explicitly linking them to the new regulatory timeline. The scale of these announcements, detailed in the table below, is notable.

The speed and scale of these announcements suggest that, for at least some groups, the regulatory shift has prompted genuine strategic recalibration. This is a welcome development for investors who have long pushed for more disciplined capital allocation. In market commentary, some analysts(3) have flagged the emergence of "stock swap" arrangements between friendly conglomerates(4) and issuance of EBs backed by treasury shares(5) as potential preemptive manoeuvre to "park" voting power before the law takes full effect.

Why this matters for global investors

The cumulative effect of Korea's three-wave reform sequence is meaningful. Directors now owe a direct fiduciary duty to shareholders, not just to the company. Boards are therefore structurally more accountable. And the treasury share channel, historically one of the most opaque instruments of entrenched control, is being systematically closed.

For international investors, the significance goes beyond any individual measure. The persistence of a significant Korea discount has always rested on a cluster of structural concerns: weak minority protections, opaque capital allocation, and the perception that even legitimate shareholder pressure could be neutralised through insider manoeuvres. The treasury share reforms, in particular, address the capital allocation dimension directly, requiring that repurchased shares be retired rather than recycled as instruments of control.

What next?

After several rapid waves of policy making, the true test will lie implementation and enforcement. The disclosure requirements around third-party disposals are only as effective as the regulatory appetite to scrutinise them. The courts will also need to define the boundaries of the amended duty of loyalty in the treasury share context, particularly in cases involving M&A and related-party transactions.

As mentioned earlier, legislative attention is now slowly turning to the BJR. In practice, lobbying efforts are already well underway. Business groups have engaged directly with stakeholders, and early draft proposals are already circulating in the National Assembly. However, some of the concepts emerging from these discussions have been criticized as potentially too broad and if adopted could significantly limit the scope of legal recourse for shareholders under the amended duty of loyalty. The final statutory language remains unsettled. How the BJR is drafted will determine whether the liability architecture built by the first and third waves remains intact.

The broader reform agenda is also moving. In a recent meeting with analysts, institutional investors and listed companies, President Lee reiterated his administration's commitment to addressing the Korea discount, with the Financial Services Commission signalling specific plans to restrict so-called "dual listings", a practice whereby chaebols list core or high-growth subsidiaries separately, to the detriment of shareholders in the parent company(6).ACGA will continue to engage constructively with regulators and policymakers as governance developments unfold in Korea, while publishing further analysis as the implementation picture becomes clearer.

Footnotes

1. https://www.kedglobal.com/regulations/newsView/ked202507110001

2. https://www.koreatimes.co.kr/business/companies/20201222/business-law-revision-hurts-firms-fighting-hostile-funds

3. https://www.businesspost.co.kr/BP?command=article_view&num=413497

4. https://biz.chosun.com/stock/stock_general/2025/09/30/SYEVKZ7RPJE5PA52XLRQDLXPDQ/

5. https://www.chosun.com/english/industry-en/2025/07/01/4JJ5CD4J2NC5TNPSONA7DRBMQQ/

6. https://www.koreaherald.com/article/10697257

About the Author(s)

Yura Ahn

Yura Ahn

Research Head, Korea, ACGA

Yura Ahn is Korea Research Head at ACGA, focusing on corporate governance research and advocacy for the market. A corporate governance and investment stewardship professional, she has nearly a decade of experience spanning buy-side, research, and advisory roles across Asia. Most recently as Korea lead analyst at BlackRock Investment Stewardship, Yura led engagements with flagship portfolio companies covering over 80% of BlackRock's regional equity exposure, while executing proxy voting on 1,000+ matters annually and advising institutional clients on stewardship outcomes.

Prior to BlackRock, Yura served as Senior Corporate Governance Consultant at IHS Markit (now S&P Global) and Analyst at Korea Corporate Governance Service (KCGS). She holds a B.A. in Business Administration from Korea University.

Download File Disclaimer

In addition to the ACGA website disclaimer access to the "Members' Area" of the ACGA website is subject to the general disclaimer and content attribution statements below.

General Disclaimer

By logging into our Members' Area you acknowledge that all materials displayed on the site or made available for download are for the exclusive use of ACGA members. You may not share the content with parties outside of your organisation.

Content Attribution

The copyright ownership of all material on our website belongs to ACGA. Should you wish to use any materials in the course of your corporate research, including directly quoting or paraphrasing sections, reprinting, reproducing or the like, we request that you give proper acknowledgement to ACGA and share a copy with us. Please email mikky@acga-asia.org.