Balancing ease and oversight: decoding India's RPT Reforms

by Anuja Agarwal, Research Head, Japan and India (edited by Dr. Helena Fung, Head of Research and Advocacy)

Related Party Transactions (RPTs) are undertaken between a company and parties related to it, including subsidiaries, but also promoters 1, key management personnel, or entities controlled by related parties. These transactions come in many forms including sales, purchases, loans, asset transfers, as well as guarantees and other financial arrangements.

In India, the significance of monitoring RPTs is particularly pronounced due to the high concentration of promoter ownership in listed companies 2. Promoters often hold majority stakes and exercise substantial control, giving rise to the risk that RPTs may be used as tools for tunnelling—transferring value out of the company to benefit insiders at the expense of minority shareholders 3. High-profile corporate failures linked to RPT misuse in India and globally underline these risks; the Enron scandal in the U.S. and the Satyam Computer Services fraud in India serve as stark reminders 4 . In Satyam’s case, the company engaged in suspicious RPTs with firms controlled by the promoters, which concealed the company’s true financial position and precipitated a collapse once the fraud was uncovered. Such cases highlight how RPTs, when misused, contribute to earnings mismanagement and loss of investor value and trust.

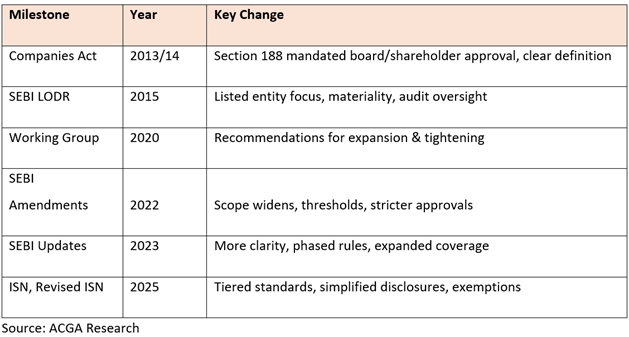

Evolution of RPT norms in India since 2013

The regulatory evolution of RPT norms in India has been marked by increasing stringency since 2013 as summarized in the table below (Table 1). The recent establishment of a dedicated open access portal for RPT analysis set up under SEBI guidance by domestic proxy advisory firms is both reflective of the prevalence and importance of RPTs in the Indian market and a welcome tool for investor awareness and analysis 5 .

Table 1: Evolution of RPT regulatory provisions since 2013

Research indicates the positive impact stemming from the introduction of stricter regulations in India. A study 6 analysing 78 non-financial companies showed a significant increase in the disclosed value of RPTs after the Companies Act 2013 came into effect, signalling improved compliance and transparency. The average annual value of RPTs reported during 2013-2015 was markedly higher than in the preceding period (2009-2012), reflective of both increased reporting and potentially better visibility of these transactions in financial statements. Group companies, characterized by concentrated ownership and multiple subsidiaries, not surprisingly reported higher values of RPTs compared with standalone firms.

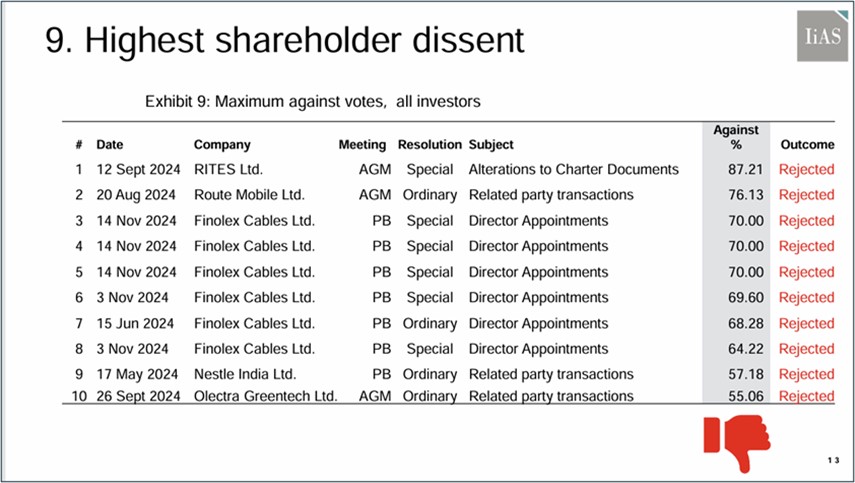

The chart below provided by IiAS 7 (Institutional Investor Advisory Services) presents a sample of proposals rejected by shareholders during the 2024 proxy season, some of which relate to RPTs.

Even in instances where RPTs are approved by shareholders, recent high-profile cases in India involving companies such as Hyundai, Paytm and Linde India, have placed renewed attention on governance challenges. These transactions have been scrutinized for their scale, terms and impact on minority shareholders, reinforcing the necessity of robust frameworks which balance business efficiency with investor protection, demonstrating the importance of this topic for corporate India.

1) Hyundai Motor India RPTs (2025)

Hyundai Motor India (HMI) sought shareholder approval for RPTs worth over Rs 31,000 crore (approximately US$ 3.5 billion) 8, nearly 40% of its annual revenue. Major transactions included a Rs 12,525 crore (US$1.4 billion) deal with Mobis India, which has no clients other than HMI, raising concerns about transparency and whether the arrangements were of genuine benefit to shareholders. Another deal with Hyundai Engineering & Construction (HEC) India LLP, a small affiliate with minimal assets and employees, involved contracts worth Rs 3,000 crore (US$ 340 million). Proxy advisory firms questioned whether HEC had the financial capacity to manage this capital or was merely a pass-through entity and whether the transaction conflicted with shareholder interests. These transactions sparked intense scrutiny over pricing, independent valuation and governance practices at Hyundai India.

2) Paytm RPT scrutiny (2024)

SEBI issued an administrative warning to One 97 Communications Limited (Paytm’s parent company) after scrutiny of RPTs involving Paytm Payments Bank Ltd. This case demonstrates SEBI’s increasing regulatory oversight of RPT disclosures and approval processes, aiming to protect minority shareholders and promote transparency in listed companies’ dealings with related parties.

3) Linde India RPT controversy (2024)

Linde India faced regulatory challenges when shareholder approval was required for material RPTs but the company attempted to proceed with transactions despite shareholder opposition. SEBI reinforced strict compliance with RPT rules, emphasizing that shareholder approvals are critical and transactions cannot bypass these legal requirements. This situation indicates increased regulatory vigilance over RPT governance and the need for companies to align with shareholders via formal approval mechanisms.

SEBI consultation on RPTs and “Ease of doing business”

On August 4, 2025, SEBI released a consultation paper proposing amendments to the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, and related circulars. The proposals aim to streamline compliance for companies while strengthening the governance of Related Party Transactions (RPTs) and protecting minority shareholder rights. This initiative aligns with the regulatory focus on "Ease of Doing Business."

Given India’s concentrated corporate ownership and historical misuse of RPTs, which attract significant scrutiny from global investors, the consultation seeks to balance reduced administrative and compliance burdens with robust oversight. Insufficient oversight could limit minority investors' access to critical information, potentially hindering informed investment and voting decisions.

Below, we outline SEBI’s proposals and provide our perspective on the amendments.

Proposal 1: Materiality thresholds

Proposal: Introduce scale-based thresholds for material RPTs linked to a company’s annual consolidated turnover to replace the flat Rs 1,000 crore or 10% turnover threshold. The tiered thresholds are:

- Up to Rs 20,000 crore (US$ 2.28 billion): 10% of turnover

- Rs 20,001-40,000 crore: Rs 2,000 crore (US$ 230 million): + 5% of turnover above Rs 20,000 crore

- Above Rs 40,000 crore: Rs 3,000 crore + 2.5% of turnover above Rs 40,000 crore, capped at Rs 5,000 crore (US$ 570 million)

- Adopt a multi-metric approach to identifying material transactions, incorporating the lower of 10% of turnover, net assets and net worth or Rs 5,000 crore, as a proportionate approach to shareholder oversight and transparency.

- Strengthen audit committee independence and limit multiple board memberships.

- Empowering audit committees to request more information for smaller exempt transactions even where these are within scope of the proposed thresholds.

- Consider introducing a dual threshold for royalty payments.

1. A term denoting controlling shareholders in an Indian context.

3. Aharony J., Wang J., Yuan H. (2010). Tunneling as an incentive for earnings management during the IPO process in China. Journal of Accounting and Public Policy, 29, 1–26. Crossref Google Scholar Auditors in on Satyam Fraud: CBI. (2009, December 7). Mint. https://www.livemint.com/Home-Page/jS33BnPzXSMnwbx9cFtplN/Auditors-in-on-Satyam-fraud-CBI.html. Google Scholar Berkman H., Cole R. A., Fu L. J. (2009). Expropriation through loan guarantees to related parties: Evidence from China. Journal of Banking & Finance, 33, 141–156.

4. https://www.scirp.org/journal/paperinformation?paperid=30220

6. (PDF) Analysis of related party transactions in India: A group and non-group company perspective

7. 2024 Shareholder Meetings Review Data

8. 1 crore rupees (which is Rs 10,000,000) equals about US$114,500. Rs 8.73 crore is US$1m at the current conversion rate.

9. SEBI | Report of the Working Group on Related Party Transactions

11. OECD Corporate Governance Factbook 2023 (EN) , Flexibility and Proportionality in Corporate Governance (EN)

12. Regulation 23(1A) states that payments made to a related party for brand or royalty usage will be considered material, and thus require shareholder approval, only if such payments exceed 'five per cent of the annual consolidated turnover of the listed entity.

14. Sebi Chief Advocates for Enhanced Roles of Independent Directors in Corporate Governance, ETCFO

About the Author(s)

Anuja Agarwal

Anuja Agarwal

Research Head, Japan and India, ACGA

Anuja Agarwal has joined ACGA to help in Advocacy and Research for Japan and India. Anuja finished her MBA from IIMA in 2004 and joined BoFA in Hong Kong. She worked successfully on sell side as a derivatives prop trader and made markets for vanilla and exotic derivatives. She had a break from Wall Street with three young kids and ran a small startup on financial literacy where she was featured on Forbes, SCMP, Radio HK. Since 2016 she joined a multimanager quant fund and since then has worked in senior buyside roles at funds. She is passionate about integrating ESG strategies with fundamental views and has experience in PRI Disclosures, Stewardship and Proxy voting. She has been a mentor for Amber Foundation, 100WF and a Board advisory for a reusable cutlery company Recube.hk. She is a ESG CFA certificate holder and a Talent4Impact Fellow. She is a fitness freak and has completed Greenpower (50k), Moon trekker (42k), UNICEF (20k) races.

Download File Disclaimer

In addition to the ACGA website disclaimer access to the "Members' Area" of the ACGA website is subject to the general disclaimer and content attribution statements below.

General Disclaimer

By logging into our Members' Area you acknowledge that all materials displayed on the site or made available for download are for the exclusive use of ACGA members. You may not share the content with parties outside of your organisation.

Content Attribution

The copyright ownership of all material on our website belongs to ACGA. Should you wish to use any materials in the course of your corporate research, including directly quoting or paraphrasing sections, reprinting, reproducing or the like, we request that you give proper acknowledgement to ACGA and share a copy with us. Please email mikky@acga-asia.org.