Hong Kong’s CG code revisions: Incremental, not revolutionary

by Lake Wang, Research Head, Greater China

Hong Kong’s stock exchange concluded its CG consultation on 19 December, moving forward with all proposed changes – though with some notable adjustments. The effective date, however, has been pushed back six months from 1 January to 1 July 2025.

It is refreshing to see that HKEX requires issuers to enhance gender diversity on the nomination committee (NC) as part of a wider set of rule changes on board and workforce diversity. A hard cap on six directorships for an INED is also welcomed. However, allowing a six-year transition period for phasing out long-serving INEDs but with an effective date starting mid-2025 is generous to issuers, essentially giving some (ie, companies with a December 31 financial year-end) over seven years from now to be rid of overly-tenured INEDs. The consultation paper had suggested a three-year implementation; the current arrangements indicate a lack of perceived urgency in addressing this issue.

It is also disappointing that having a Lead INED is merely a recommended best practice (RBP), which essentially means corporates can ignore this and do not need to provide any explanation to shareholders. ACGA members will be particularly disappointed, given the growing investor demand for direct dialogue with INEDs to take corporate governance beyond just compliance which most Hong Kong-listed companies see it as.

A light touch on Lead INEDs

Appointing a Lead INED in the absence of an independent board chair has been endorsed in RBP C.1.8, but this is a step back from the proposed code provision in the consultation which had been for this to be on a “comply or explain” basis. Issuers are, however, mandated to disclose “details of shareholder engagement,” including the nature and frequency of engagements, as well as the “approach” taken to address any investor concerns (MDR paragraph L(d), CP F.1.1). At ACGA, we believe having a designated Lead INED is key for meaningful engagement between investors and independent directors (INED) on governance and board practices, hence we are disappointed this did not get stronger backing by the regulator. Issuers are free to, and often do, simply ignore RBPs.

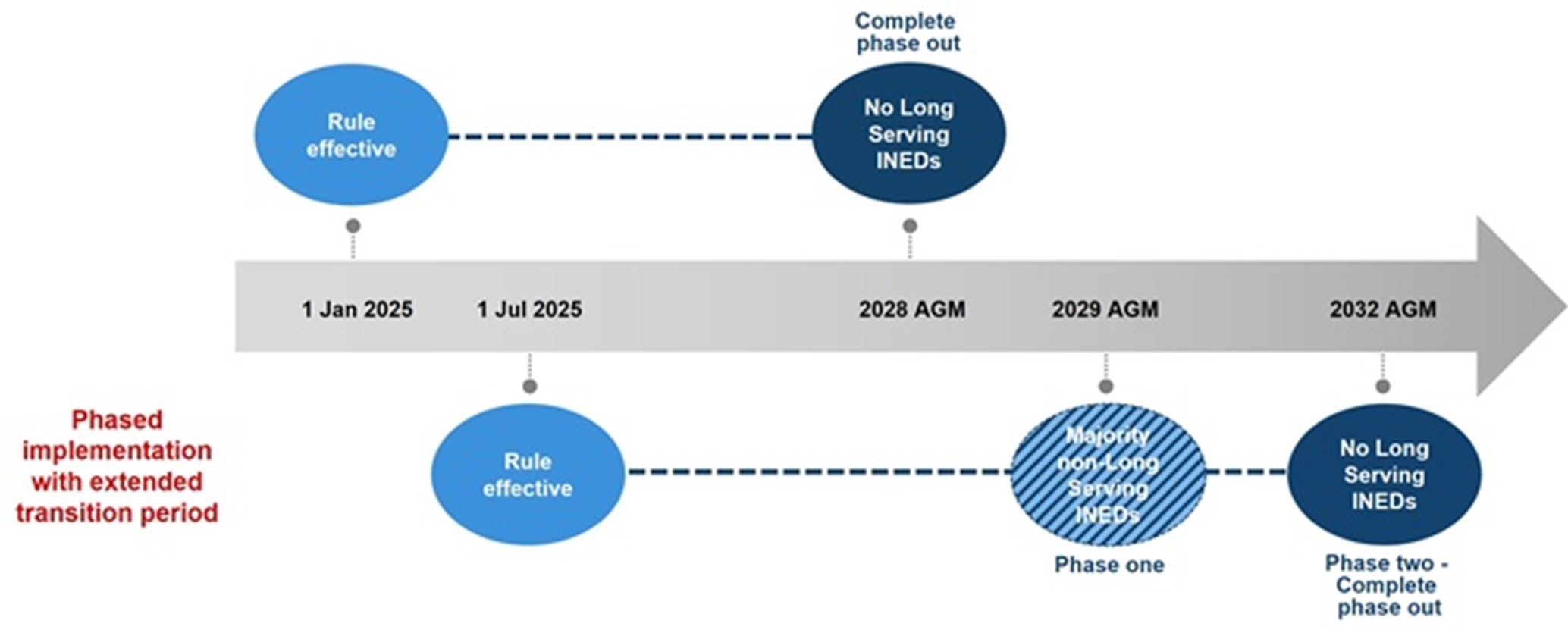

A long goodbye to long-serving INEDs

The nine-year hard cap on INED tenure is now a listing rule (3.13A), and the cooling-off period has been extended from the initial proposal of two years to three. However, implementation will be phased in over six years, rather than the originally proposed three years to implement.

As at the conclusion of the first AGM on or after 31 July 2028, long-serving INEDs will no longer be able to constitute a majority of the INEDs on any Hong Kong listed company board. Any remaining overstayers must be replaced as at the conclusion of the first AGM held on or after 1 July 2031. In effect, entrenched INEDs will be completely phased out as at the conclusion of 2032 AGMs for companies with a December 31 financial year-end – more than seven years from now!

Illustration for December financial year-end issuers

Source: HKEX

Of the 24 named issuers who disclosed their submissions, only MTR and Guotai Junan International fully supported the nine-year rule and the three-year transition period. Other companies opposed the hard cap of nine years tenure for INEDs.

Other notable improvements in the Code and related listing rules:

• Hard cap on overboarding. Newly introduced rule 3.12A limits the number of listed company directorships an INED can hold to six, with a three-year transition period. Furthermore, companies seeking IPOs will be barred from having overboarded INEDs from 1 July 2025.

• Board diversity. A new code provision (B.3.5) requires issuers to appoint at least one female director to their NC. Issuers must also annually review and disclose the implementation of their board diversity policy, which “should” include targets and timelines (MDR paragraph J).

• Dividends. Issuers are mandated to disclose their dividend policies (MDR paragraph M). HKEX encourages issuers to “go beyond what is required in Listing Rules” (the consultation conclusions, p32) to enhance shareholder value, noting China’s recent guidelines on market value management and similar developments in the region.

• Board evaluation. Conducting a board evaluation at least every two years is now a code provision (B.1.4), upgraded from a RBP. Evaluation findings are required to be publicly disclosed. Yet HKEX emphasises that the exercise should focus on the board’s overall performance rather than “a personal assessment of individual directors” (p18) and it does not require external board evaluations.

• Skills matrix. Issuers are required to maintain and disclose a skills matrix under the new CP B.1.5. However, this provision does not differentiate between the matrix for INEDs/NEDs and that for executive directors.

• Director training. New directors without directorship experience at companies on other exchanges must receive at least 24 hours of training within one and half years of their appointment, while those with such experience require at least 12 hours (listing rule 3.09H). Issuers must also disclose details of each director’s continuous professional development (MDR paragraph B). There is still no requirement regarding the format of training.

• Risk management. An annual review of risk management and internal control systems (RMIC systems) is now subject to mandatory disclosure (MDR paragraph H). HKEX highlights that external reviews remain at the issuer’s discretion (p16).

Missed opportunities for Hong Kong to be a CG leader

About the Author(s)

Lake Wang

Lake Wang

Research Head, Greater China, ACGA

Lake Wang joined ACGA in October 2023. He supports ACGA’s research on corporate governance and ESG development in 12 Asia-Pacific markets, with a focus on Greater China. Before joining ACGA, Lake worked for an equity hedge fund for over five years. Additionally, he conducted research at global professional services firms and in academia.

Download File Disclaimer

In addition to the ACGA website disclaimer access to the "Members' Area" of the ACGA website is subject to the general disclaimer and content attribution statements below.

General Disclaimer

By logging into our Members' Area you acknowledge that all materials displayed on the site or made available for download are for the exclusive use of ACGA members. You may not share the content with parties outside of your organisation.

Content Attribution

The copyright ownership of all material on our website belongs to ACGA. Should you wish to use any materials in the course of your corporate research, including directly quoting or paraphrasing sections, reprinting, reproducing or the like, we request that you give proper acknowledgement to ACGA and share a copy with us. Please email irina@acga-asia.org.